Brexit Squared – What Trump’s Victory Means for Bonds

Our initial observation is that Globalization has run into a wall. Brexit in the UK and the election of a right wing Republican president running on a platform of protectionism and immigration reforms demonstrates a very important global trend that we believe will continue in the upcoming European elections.

Nationalistic and protectionist policies are beginning to prevail not only at the top echelons of government but through popular Democratic uprisings, more importantly, through democratically sanctioned popular votes that demonstrate a shift in behavioral psychology and public mindset. Financial markets need to understand this and react and adapt accordingly.

Nationalist and protectionist policies are highly probable going forward, which ultimately is bad for corporate profits, however, there are certain considerations before coming to that conclusion that need to be examined.

In theory, a Trump victory should be bad for European Credit, we believe, however, that continued intervention by the ECB and a continued bond buying combined with a yield hungry investment universe will offset any negative impact as a result of continued improved technicals in the hunt for yield

Looking towards the future, we should not completely rule out a victory for Marine Le Pen in the French elections, we should also not rule out a seismic shift in the German elections and we should prepare ourselves for a change of regime in Italy.

What does this mean for the financial markets?

The key is fiscal policy, the rationale goes something like this, monetary policy has achieved everything it can negative rates or zero interest rates have not brought forward consumer demand as the economic textbooks would have us believe.

Common economic theory points to increased government spending as the second form of stimulus that is necessary, i.e. infrastructure projects, airports, roads, etc., as well as healthcare and other forms of social redistribution which increase the general public’s disposable income bringing forward investment decisions that may have been put off due to saving ratios and purchasing power parity.

Put simply, we believe that a Trump victory will be better for bonds as a result of moderate fiscal expansionist policy by the US government combined with protectionist policies having a diminishing effect on inflation, and US domestic corporate growth.

A Trump victory is unlikely to suddenly stimulate growth, regardless of the fiscal rhetoric we have seen, protectionist policies will dampen US corporate growth, immigration policies will reduce cheap labor and increase production and unit output costs, potentially we might see wage inflation as a result of the reduction of cheap imported labor. We believe therefore that markets need to carefully observe the balance between the effect of moderate fiscal policy and protectionist and nationalistic domestic policy against the potentially inflationary impact of a reduction in imported labor.

Therefore, the anticipation is that a lower rate environment for longer combined with some dampening of inflation leads to a flatter yield curve over a longer period of time. The key variable is inflation, which will be impacted by the magnitude of fiscal policy in the US.

Emerging markets will be negatively affected as imports, immigration, and many of the policy decisions articulated by Trump are good for US businesses, but bad for companies in countries that export into the US domestic market. Look below at the short term impact of a Trump victory on the Mexican peso a major trading partner to the US. This is the quantifiable visualization of protectionist policies affect on Mexico.

In terms of sector rotation, analysis points to the fact that a Trump victory is:

· Good for coal and the energy complex

· Bad for energy alternatives

· Bad for autos

· Good for financial services due to looser regulation

· Good for defence spending

· Cyclical stocks underperform

· Defensive stocks outperform

· Good for bonds

· Moderate or perhaps bad for equities

On this last point, it depends very much on the relative yield via dividends of the S&P as compared to bonds. If bond yields stabilize and remain low, then equity prices have to come down in order for dividend yields to compare favorably to the returns you could get from the alternative, i.e. bond investments. As growth expectations are reduced due to protectionism bond yields become more attractive than dividend yield in equities due to repricing of equity market on the back of lowered growth expectations for US.

See below. The initial impact a Trump victory had on the S&P 500. We believe these losses will be erased in the near-term. However, the initial reaction demonstrates the overriding concern and trend.

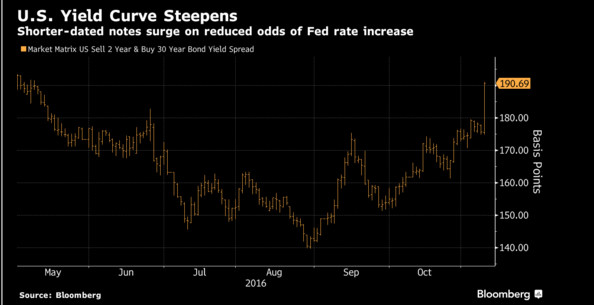

The likelihood of an interest rate rise in December has significantly diminished. Given the Trump victory, indicating that lower for longer is probably the anticipated outcome and mindset of the Federal Reserve. Below is the price of short-term debt after the vote. i.e., higher price equals lower yield. The graph below demonstrates the immediate reaction of short-term rates to a Trump victory, prices of treasuries have gone up as the expectations of a December rate rise have diminished significantly, indicating lower short-term rates for longer.

The probabilities associated with an interest rate hike in December were 86% for a Clinton victory and 26% probability for a Trump victory

Conclusion

A Republican president with a majority in the House and Senate can and will be effectual in terms of implementing public policy specifically fiscal reforms. Fiscal reforms are key to the future growth trajectory of the US and interest rates/inflation/the shape of the bond curve, however, a Republican candidate having won on a platform of protectionism and immigration controls is much less likely to massively stimulate fiscal policy as we would have seen had Clinton won the election.

We believe a Trump victory will lead to a more moderate longer-term steepening of the yield curve with control on inflation due to domestic protectionist policies, moderate fiscal stimulus, and moderate growth in the US.

Please feel free to comment and contact us with any questions

lg@lngcapital.com +442078393456 www.lngcapital.com